APMs Overview

Implement local payment rails like bank transfers & QR schemes. Our guide covers asynchronous payment flows, customer redirects, and receiving final payment status via webhook notifications.

Alternative Payment Methods (APMs) are local, bank-native or scheme-specific rails; such as instant bank transfers, QR schemes, and account-to-account flows that let customers pay from their own banking app or wallet without entering card data. APMs are typically asynchronous: customers complete steps outside your checkout (redirect/QR/app handoff) and your system receives the final state via webhooks. APMs often deliver higher reach and approval rates, lower fees than cards, and strong local trust.

Supported Countries & Coverage

APM processing is available in the following countries:

Use Cases

Offer a pay-by-bank experience customers already trust, reducing friction and card declines—ideal for high AOV and banked populations.

Present dynamic QR codes or app deep links so customers approve payments in their banking or wallet apps.

Online retailers expanding into new markets can instantly offer locally preferred payment methods without building separate integrations.

Platforms paying contractors globally can leverage local payout methods through the same APM infrastructure. Workers receive funds through their preferred payment channels—whether bank transfers, digital wallets, or cash pickup locations—improving satisfaction and reducing payout costs.

How It Works

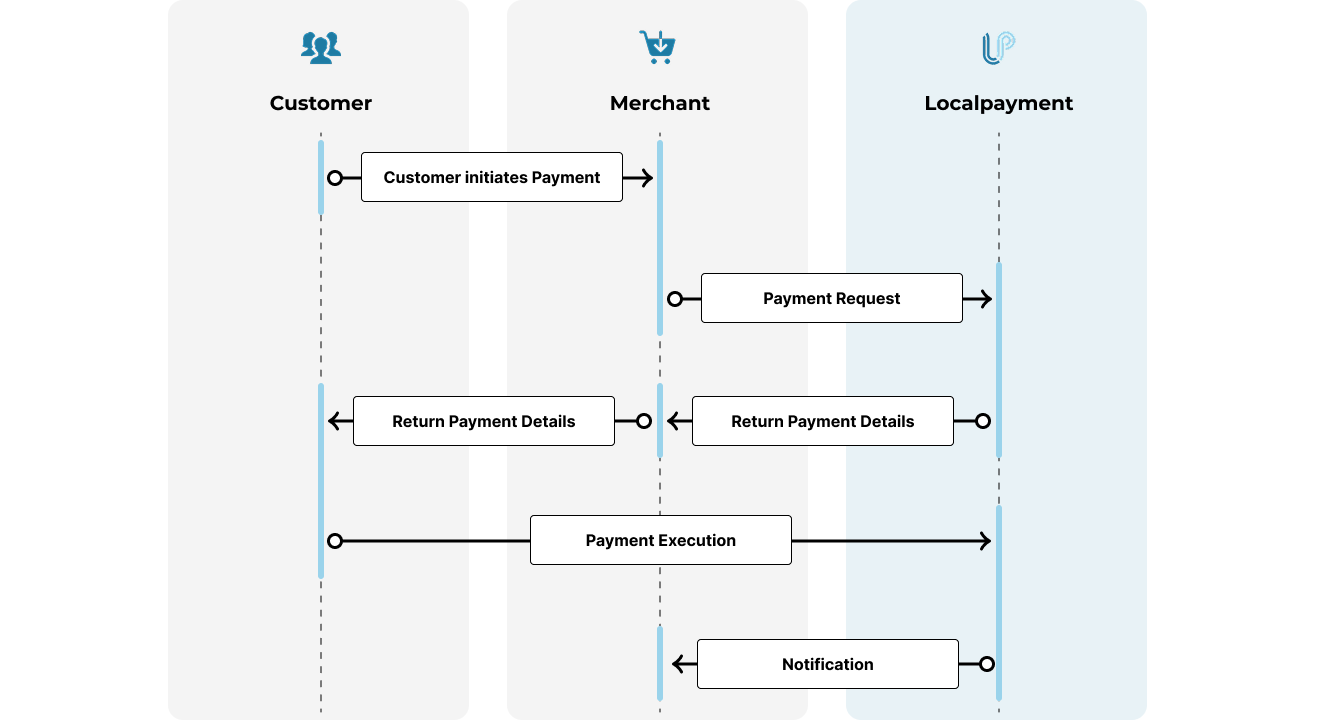

The process of integrating and using Alternative Payment Methods through Localpayment involves the following steps:

- Customer Initiates Payment: Your customer selects the payment option within your application's checkout flow.

- Payment Request: Your application securely gathers the necessary payment details and submits them to Localpayment's API to initiate the transaction.

- Return Payment Details: Localpayment returns a response containing the payment information and instructions. In case of an error, a message detailing the issue is provided.

- Payment Execution: The customer completes authentication through their chosen method and authorizes the payment.

- Notification: Once the payment is made, the merchant is notified, and the order is processed.

Prerequisites

Before offering Alternative Payment Methods to your customers, ensure you've completed these essential requirements:

Implementation Guide

Implementing Alternative Payment Methods enables you to capture more revenue by meeting local payment preferences while maintaining a unified technical integration. Below are the key implementation workflows:

Accept instant payments through Argentina's standardized QR payment system. Customers scan dynamic QR codes with their mobile banking apps to authorize transfers in real-time, providing immediate payment confirmation and reducing transaction abandonment.

Argentina's real-time direct debit system enabling instant payment requests between bank accounts. Process one-time or recurring payments with immediate customer authorization through their online banking platform.

Process payments via Bolivia's interoperable QR payment network. Generate static or dynamic QR codes that customers can scan with any participating bank app, enabling instant bank transfers without card networks or manual data entry.

Brazil's instant payment system enabling 24/7 real-time transfers between any bank accounts. Offer Pix via QR codes, payment links, or copy-paste codes with immediate settlement and the lowest processing fees in the Brazilian market.

Chilean payment gateway specializing in local bank transfers and alternative payment methods. Process payments through Webpay and other local systems with automatic reconciliation and multi-bank settlement capabilities.

Colombia's national real-time A2A payment system operated by Banco de la República. Receive instant bank transfers 24/7 through a unique Bre-B key — no redirect required. Interoperable across all Colombian banks, digital wallets, and cooperatives.

Colombia's secure online banking payment system that redirects customers to their bank for authentication. Process payments in real-time with immediate confirmation and support for all major Colombian banks through a single integration.

Guatemala's central bank-regulated QR payment system for instant interbank transfers. Generate standardized QR codes that work across all participating Guatemalan banks, providing unified payment experience with instant settlement.

Guatemala's Wallet Fri system for direct bank account debits through authorized mandates. Collect payments from customer bank accounts with pre-approved authorization for recurring billing scenarios.

Mexico's real-time digital payment system operated by Banco de México. Process instant bank transfers via QR codes or dynamic links with immediate settlement and confirmation, leveraging Mexico's SPEI infrastructure for secure 24/7 payments.

APM Operations

Once APMs are configured, you can manage various operational aspects throughout the payment lifecycle. The available features and capabilities depend on the specific payment method, country regulations, and technical requirements. Here's an overview of key operational capabilities by region:

Updated about 1 month ago